The Boston Globe hits on something important in an editorial today, reminding the president that he was elected with a rather broad mandate and he should not be letting three Republicans — so-called moderates — dictate what the federal stimulus package looks like.

That essentially is what has happened so far, as he attempts to wrangle bipartisan support behind the massive federal spending plan.

And yes, this is a spending plan. The idea behind any stimulus is to get money into the economy; the way you do that is to spend it. You can argue over the efficacy of public works projects, aid to states and tax rebates, but the simple fact is all of them are spending measures.

That said, the Globe makes a few good points — most notably, the aforementioned headcount.

With backing from only three Republicans – Senators Susan Collins and Olympia Snowe of Maine and Arlen Specter of Pennsylvania – the Senate yesterday passed an $838 billion stimulus bill that calls for about $108 billion less in spending than the House version. Unfortunately, the Senate plan eliminates $40 billion in state aid, much of it targeted for education. The same three Republicans who voted for the Senate plan also helped draft it and took the money out.

The reason, The Globe implies, is that the GOP has taken control of the narrative.

The point of the stimulus bill is to keep money moving through the economy – by blunting the impact of the recession upon individual families, and by creating jobs through public investments that produce long-term benefits. Yet to GOP critics, if it’s not a tax cut, it’s pork.

Pork, of course, is a bad word in politics, but “One person’s pork is another person’s beef.” The cuts in aid to states for a variety of state-level programs made by the Senate at the expense of new tax cuts have triggered a backlash among governors, leading Republicans like Arnold Schwartzenegger and Charlie Crist — one of John McCain’s closest allies — to get behind the new president.

Consider this photo from The Herald Tribune (via The New York Times):

The Globe notes Crist’s support, adding that

he introduced Obama at yesterday’s town hall meeting in Fort Myers, Fla. “This is not about partisan politics. It’s about rising above that, helping America and reigniting our economy,” Crist said.

The states, as most governors admit, “play a crucial role in reigniting the economy,” but most face budget shortfalls — some that make New Jersey’s look like pocket change.

If the federal government doesn’t come through for them, state workers will lose their jobs and state services will continue to decline, hurting the most vulnerable.

Obama, as The Globe writes, needs to take control of this debate, especially with negotiators from both house of Congress hacking away at the package in an attempt to come to a compromise.

The differences in the two plans — outlined in a nice chart from ProPublica (referenced by David Sirota on Open Left) — are pretty stark and encapsulate the differing priorities of the people running the show in their respetive houses. The House, not having to face a potential filibuster, offers a more comprehensive and progressive plan, with significant money for education, energy efficiency, aid to states and the poor. The Senate, which has been hijacked by the three Republican moderates and a few Bluedog Democrats, slashed much of this aid from the bill.

The Senate bill cut $27 billion from aid to the poor, $37.7 billion from aid to the states, $25.6 billion from education (mostly in school construction) and $14.7 billion from energy (which includes an $4.5 billion increase in spending on fossil fuel research, meaning cuts to alternative energy equal $19.2 billion). In their place, the Senate added $75.9 billion in tax cuts.

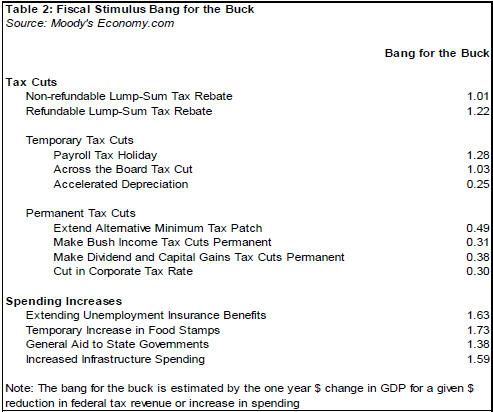

These numbers need context, of course, which has been supplied by Moody’s, the investment service. Moody’s, citing “a new policy consensus … forged out of collapse,” called for “aggressive and consistent action to quell the panic and mitigate the economic fallout.”

An unfettered Federal Reserve will pump an unprecedented amount of liquidity into the financial system to unlock money and credit markets. The TARP fund will be deployed more broadly to shore up the still-fragile financial system, and another much larger and comprehensive foreclosure mitigation program is needed to forestall some of the millions of mortgage defaults that will occur otherwise. Finally, another very sizable economic stimulus plan is vitally needed.

According to Moody’s, the House package offered “a very good starting point.” While the costs to the Treasury will be substantial, Moody’s said, the potential negative consequences “are problems for another day.”

The key finding, however, is that

Increased government spending provides a large economic bang for the buck and thus significantly boosts the economy. The benefits begin as soon as the money is disbursed and are less likely than tax cuts to be diluted by an increase in imports. The most effective proposals included in the House stimulus plan are extending unemployment insurance benefits, expanding the food stamp program, and increasing aid to state and local governments. Increasing infrastructure spending will also greatly boost the economy, particularly as the current downturn is expected to last for an extended period. Most of the infrastructure money will be spent on hiring workers and on materials and equipment produced domestically.

At the same time,

Tax cuts generally provide less of an economic boost, particularly if they are temporary; on the other hand they can be implemented quickly. A particular plus for individual tax cuts included in the House stimulus plan such as the payroll tax and earned income tax credits is that they are targeted to benefit lower- and middle-income households that are more likely to spend the extra cash quickly. Investment and job tax benefits for businesses are less economically effective, but are not very costly and more widely distribute the benefits of the stimulus plan.

Moody’s offers a nifty little chart (chart taken from Open Left), which assigns value to each element of the stimulus plan:

I know a mediocre bill is better than no bill, but a failed bill likely will lead to retrenchment and blame and the end of the public’s limited tolerance for government intervention.